Understanding Accruals. An accrual is a record of revenue or expenses that have been earned or incurred but have not yet been recorded in the company's financial statements. This can include things like unpaid invoices for services provided, or expenses that have been incurred but not yet paid.In summary, the two main types of accruals in accounting are accrued revenue and accrued expenses, but there are other types of accruals that may be used in specific situations, such as accrued interest, accrued salaries, and accrued taxes.An accrual, or accrued expense, is a means of recording an expense that was incurred in one accounting period but not paid until a future accounting period.

What is an example of an accrual basis entry : Examples of accrual accounting include sales and purchases made on credit, income tax expenses, prepaid rent, accrued interest, insurance expenses, electricity expenses, post-sales discounts, depreciation, and audit fees.

What are the most common accruals

Common examples of accrued expenses include:

Interest Expense Accruals: These represent interest expenses that a company owes but has not yet paid.

Supplier Accruals: These are operating expenses incurred for goods or services provided by third-party suppliers on credit terms.

What is accrual simple words : Accruals are amounts of money that have been earned or spent, but not yet paid. Businesses use accruals to keep tabs on what's owed. It may be money that's going to come in, such as payment from a customer.

Accrued revenues or assets

Accrued capital expenditures is another example: a company may have received PP&E but has yet to pay for it. Example: An example of accrued revenue is electricity consumption. An electricity company usually provides the utility to its consumer prior to receiving payment for it. Common examples of accrued expenses include wages, utilities, and services received but not yet invoiced. Accrued expenses have a net positive impact on a company's free cash flow (FCF) until paid off.

How do you record accruals

How to record accrued revenue

Identify the revenue. The first step is to identify the revenue that the business has earned but for which it has not yet received payment.

Create a balance sheet entry.

Update the financial statements.

Invoice the customer.

Record the payment.

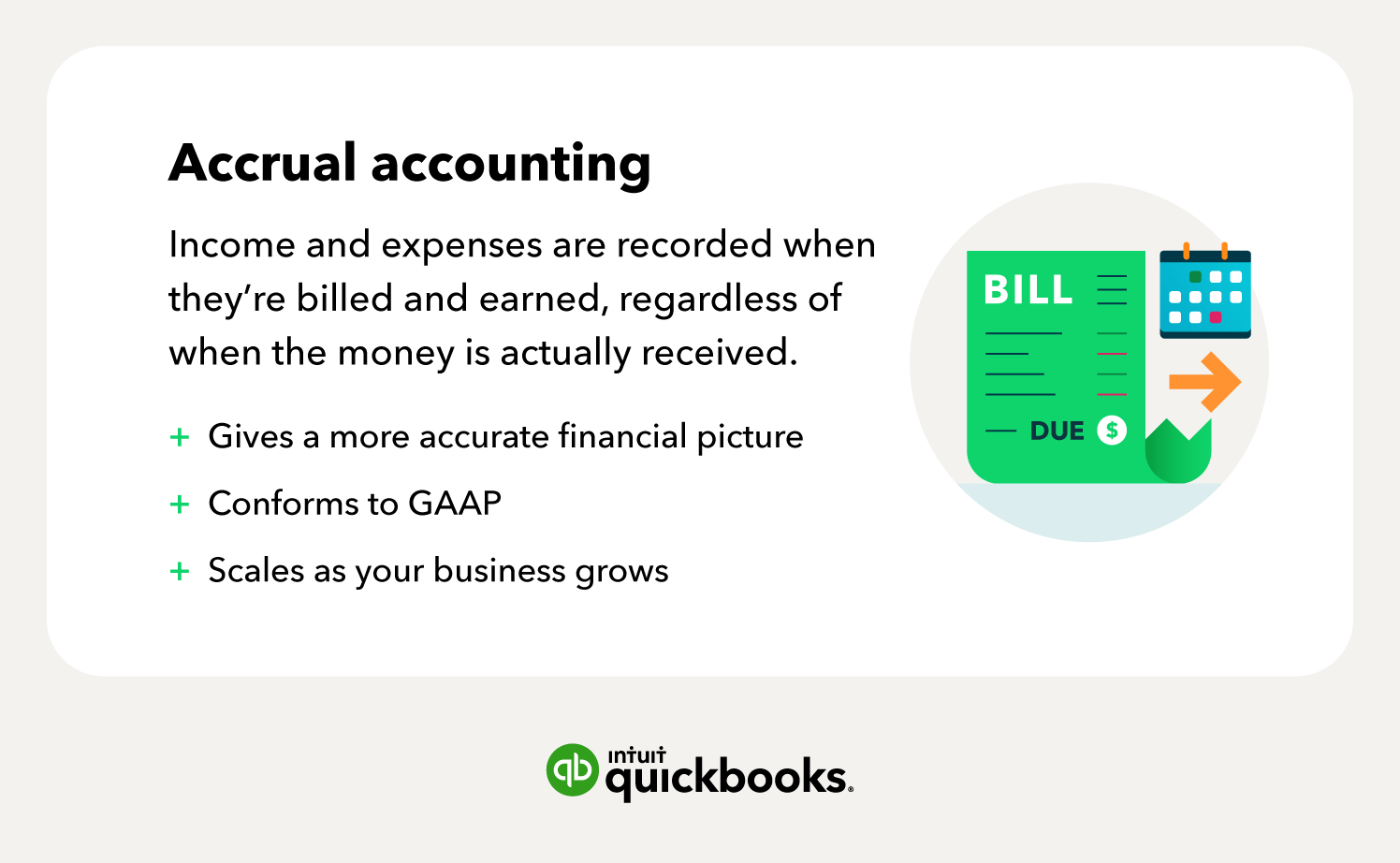

The normal accruals are preordained to capture adjustments that reflect fundamental performance, whereas abnormal accruals are inevitable to apprehend distortions induced by application of accounting rules or earnings management.Key Takeaways: Accrual accounting is an accounting method where revenue or expenses are recorded when a transaction occurs vs. when payment is received or made. The method follows the matching principle, which says that revenues and expenses should be recognized in the same period. The term "accrue," when related to finance, is synonymous with an "accrual" under the accounting method outlined by Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

What type of asset is accrued : Accrued revenues or assets

Accrued revenues are either income or assets (including non-cash assets) that are yet to be received but where an economic transaction has effectively taken place. In this case, a company may provide services or deliver goods, but does so on credit.

What expense can be accrued : Accrued expenses, also known as accrued liabilities, are expenses recognized when they are incurred but not yet paid in the accrual method of accounting. Typical accrued expenses include utility, salaries, and goods and services consumed but not yet billed.

What type of account is accrual

Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are incurred. What is an accrued expense journal entry Businesses typically use an accrued expense journal entry to record expenses incurred throughout an accounting period that they haven't yet paid during that accounting period. The expenditure account gets debited, and the accrued liabilities account gets credited.An accrued expense—also called accrued liability—is an expense recognized as incurred but not yet paid. In most cases, an accrued expense is a debit to an expense account. This increases your expenses. You may also apply a credit to an accrued liabilities account, which increases your liabilities.

How do you identify accruals : Under accrual basis accounting, revenue is recognised when it is earned and payment is assured, and the accounting should occur within the same financial reporting period.

![Kladsko-5-malý-Karlův-Most[1]](https://www.einarstrayorchestra.com/wp-content/uploads/2024/06/Kladsko-5-maly-Karluv-Most1-1024x692-250x120.jpg)

![Stubai[1]](https://www.einarstrayorchestra.com/wp-content/uploads/2024/06/Stubai1-250x120.jpg)

Antwort What are two examples of accruals? Weitere Antworten – What are accruals and give an example

Understanding Accruals. An accrual is a record of revenue or expenses that have been earned or incurred but have not yet been recorded in the company's financial statements. This can include things like unpaid invoices for services provided, or expenses that have been incurred but not yet paid.In summary, the two main types of accruals in accounting are accrued revenue and accrued expenses, but there are other types of accruals that may be used in specific situations, such as accrued interest, accrued salaries, and accrued taxes.An accrual, or accrued expense, is a means of recording an expense that was incurred in one accounting period but not paid until a future accounting period.

What is an example of an accrual basis entry : Examples of accrual accounting include sales and purchases made on credit, income tax expenses, prepaid rent, accrued interest, insurance expenses, electricity expenses, post-sales discounts, depreciation, and audit fees.

What are the most common accruals

Common examples of accrued expenses include:

What is accrual simple words : Accruals are amounts of money that have been earned or spent, but not yet paid. Businesses use accruals to keep tabs on what's owed. It may be money that's going to come in, such as payment from a customer.

Accrued revenues or assets

Accrued capital expenditures is another example: a company may have received PP&E but has yet to pay for it. Example: An example of accrued revenue is electricity consumption. An electricity company usually provides the utility to its consumer prior to receiving payment for it.

Common examples of accrued expenses include wages, utilities, and services received but not yet invoiced. Accrued expenses have a net positive impact on a company's free cash flow (FCF) until paid off.

How do you record accruals

How to record accrued revenue

The normal accruals are preordained to capture adjustments that reflect fundamental performance, whereas abnormal accruals are inevitable to apprehend distortions induced by application of accounting rules or earnings management.Key Takeaways: Accrual accounting is an accounting method where revenue or expenses are recorded when a transaction occurs vs. when payment is received or made. The method follows the matching principle, which says that revenues and expenses should be recognized in the same period.

The term "accrue," when related to finance, is synonymous with an "accrual" under the accounting method outlined by Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

What type of asset is accrued : Accrued revenues or assets

Accrued revenues are either income or assets (including non-cash assets) that are yet to be received but where an economic transaction has effectively taken place. In this case, a company may provide services or deliver goods, but does so on credit.

What expense can be accrued : Accrued expenses, also known as accrued liabilities, are expenses recognized when they are incurred but not yet paid in the accrual method of accounting. Typical accrued expenses include utility, salaries, and goods and services consumed but not yet billed.

What type of account is accrual

Accrual accounting is a financial accounting method that allows a company to record revenue before receiving payment for goods or services sold and record expenses as they are incurred.

What is an accrued expense journal entry Businesses typically use an accrued expense journal entry to record expenses incurred throughout an accounting period that they haven't yet paid during that accounting period. The expenditure account gets debited, and the accrued liabilities account gets credited.An accrued expense—also called accrued liability—is an expense recognized as incurred but not yet paid. In most cases, an accrued expense is a debit to an expense account. This increases your expenses. You may also apply a credit to an accrued liabilities account, which increases your liabilities.

How do you identify accruals : Under accrual basis accounting, revenue is recognised when it is earned and payment is assured, and the accounting should occur within the same financial reporting period.