Financial accounting. Financial accounting is a type of accounting that records, analyzes, and summarizes business financial transactions.

Management accounting.

Tax accounting.

Cost accounting.

Forensic accounting.

Public accounting.

Fiduciary accounting.

Governmental accounting.

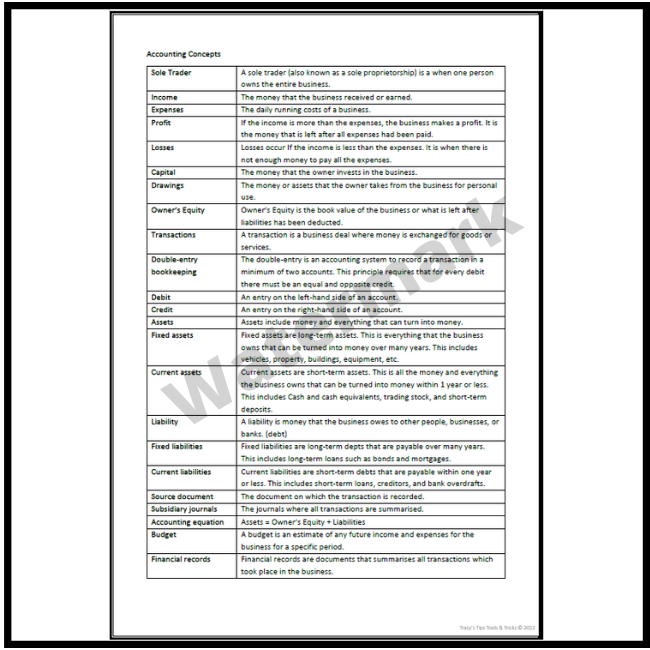

: Business Entity, Money Measurement, Going Concern, Accounting Period, Cost Concept, Duality Aspect concept, Realisation Concept, Accrual Concept and Matching Concept.Basic accounting concepts used in the business world cover revenues, expenses, assets, and liabilities. These elements are tracked and recorded in documents including balance sheets, income statements, and cash flow statements.

What are the 5 main in accounting : 5 Types of accounts

Assets.

Expenses.

Liabilities.

Equity.

Revenue (or income)

What are the 8 elements of accounting

Each company decides if they would like additional steps, but the accounting cycle typically includes these eight steps:

Identifying transactions.

Recording transactions.

Posting the general ledger.

Trial balancing.

Analyzing the worksheet.

Adjusting journal entries.

Producing the financial statements.

Closing the books.

What are the 8 branches of accounting : The eight branches of accounting include financial accounting, managerial accounting, cost accounting, tax accounting, auditing, accounting information systems, fund accounting, and international accounting. Each branch serves distinct purposes and contributes to the financial management of organizations.

Here are the 13 principles: -Accrual principle -Conservatism principle -Consistency principle -Cost principle -Economic entity principle -Full disclosure principle -Going concern principle -Matching principle -Materiality principle -Monetary unit principle -Reliability principle -Revenue recognition principle -Time … What are the 5 basic principles of accounting

Revenue Recognition Principle. When you are recording information about your business, you need to consider the revenue recognition principle.

Cost Principle.

Matching Principle.

Full Disclosure Principle.

Objectivity Principle.

What are the 3 golden rules of accounting

The three golden rules of accounting are (1) debit all expenses and losses, credit all incomes and gains, (2) debit the receiver, credit the giver, and (3) debit what comes in, credit what goes out. These rules are the basis of double-entry accounting, first attributed to Luca Pacioli.The steps in the accounting cycle are identifying transactions, recording transactions in a journal, posting the transactions, preparing the unadjusted trial balance, analyzing the worksheet, adjusting journal entry discrepancies, preparing a financial statement, and closing the books.The firms were referred to as the Big Eight for most of the 20th century, reflecting the international dominance of the eight largest firms:

Arthur Andersen.

Arthur Young.

Coopers & Lybrand.

Deloitte Haskins & Sells.

Ernst & Whinney.

Peat Marwick Mitchell.

Price Waterhouse.

Touche Ross.

What Are the Basic Accounting Principles

Accrual principle.

Conservatism principle.

Consistency principle.

Cost principle.

Economic entity principle.

Full disclosure principle.

Going concern principle.

Matching principle.

What are the 5 accounting rules : What are the 5 basic principles of accounting

Revenue Recognition Principle. When you are recording information about your business, you need to consider the revenue recognition principle.

Cost Principle.

Matching Principle.

Full Disclosure Principle.

Objectivity Principle.

What is a golden rule of account : The three golden rules of accounting are (1) debit all expenses and losses, credit all incomes and gains, (2) debit the receiver, credit the giver, and (3) debit what comes in, credit what goes out.

What are the 3 basic principles of accounting

Some of the most fundamental accounting principles include the following: Accrual principle. Conservatism principle. Consistency principle. How to Learn Financial Accounting

Learn How to Read and Analyze Financial Statements.

Select a Learning Method.

Dedicate Time to Your Learning.

Focus on Real-World Application.

Network with Other Accounting Professionals.

Overview. IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors is applied in selecting and applying accounting policies, accounting for changes in estimates and reflecting corrections of prior period errors.

What are the 8 steps in the accounting cycle PDF : Accounting Cycle Steps

![Kladsko-5-malý-Karlův-Most[1]](https://www.einarstrayorchestra.com/wp-content/uploads/2024/06/Kladsko-5-maly-Karluv-Most1-1024x692-250x120.jpg)

![Stubai[1]](https://www.einarstrayorchestra.com/wp-content/uploads/2024/06/Stubai1-250x120.jpg)

Antwort What are the 8 concepts of accounting? Weitere Antworten – What are the 8 types of accounting

: Business Entity, Money Measurement, Going Concern, Accounting Period, Cost Concept, Duality Aspect concept, Realisation Concept, Accrual Concept and Matching Concept.Basic accounting concepts used in the business world cover revenues, expenses, assets, and liabilities. These elements are tracked and recorded in documents including balance sheets, income statements, and cash flow statements.

What are the 5 main in accounting : 5 Types of accounts

What are the 8 elements of accounting

Each company decides if they would like additional steps, but the accounting cycle typically includes these eight steps:

What are the 8 branches of accounting : The eight branches of accounting include financial accounting, managerial accounting, cost accounting, tax accounting, auditing, accounting information systems, fund accounting, and international accounting. Each branch serves distinct purposes and contributes to the financial management of organizations.

Here are the 13 principles: -Accrual principle -Conservatism principle -Consistency principle -Cost principle -Economic entity principle -Full disclosure principle -Going concern principle -Matching principle -Materiality principle -Monetary unit principle -Reliability principle -Revenue recognition principle -Time …

What are the 5 basic principles of accounting

What are the 3 golden rules of accounting

The three golden rules of accounting are (1) debit all expenses and losses, credit all incomes and gains, (2) debit the receiver, credit the giver, and (3) debit what comes in, credit what goes out. These rules are the basis of double-entry accounting, first attributed to Luca Pacioli.The steps in the accounting cycle are identifying transactions, recording transactions in a journal, posting the transactions, preparing the unadjusted trial balance, analyzing the worksheet, adjusting journal entry discrepancies, preparing a financial statement, and closing the books.The firms were referred to as the Big Eight for most of the 20th century, reflecting the international dominance of the eight largest firms:

What Are the Basic Accounting Principles

What are the 5 accounting rules : What are the 5 basic principles of accounting

What is a golden rule of account : The three golden rules of accounting are (1) debit all expenses and losses, credit all incomes and gains, (2) debit the receiver, credit the giver, and (3) debit what comes in, credit what goes out.

What are the 3 basic principles of accounting

Some of the most fundamental accounting principles include the following: Accrual principle. Conservatism principle. Consistency principle.

How to Learn Financial Accounting

Overview. IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors is applied in selecting and applying accounting policies, accounting for changes in estimates and reflecting corrections of prior period errors.

What are the 8 steps in the accounting cycle PDF : Accounting Cycle Steps